| Скачать .docx |

Реферат: Financial Planing

Unit 4

Financial planning (like all planning) begins with the establishment of goals and objectives. Next, planners must assign costs to these goals and objectives. That is, they must determine how much money is needed to accomplish each one. Finally, financial planners must identify available sources of financing and decide which to use. In the process, they must make sure that financing needs are realistic and that sufficient funding is available to meet those needs.

THREE STEPS OF FINANCIAL PLANNING

1. Establishing Organizational Goals and Objectives. Establishing goals and objectives is an important management task. A goal is an end state that the organization wants to achieve. Objectives are specific statements detailing what the organization intends to accomplish within a certain period of time. If goals and objectives are not specific and measurable, they cannot be translated into costs, and financial planning cannot proceed. They must also be realistic. Otherwise, it may be impossible to finance or achieve them.

2. Budgeting for Financial Needs. A budget is a financial statement that projects income and/or expenditures over a specified future period of time. Once planners know what the firm's goals and objectives are for a specific period of time - say, the next calendar year- they can estimate the various costs the firm will incur and the revenues it will receive. By combining these items into a companywide budget, financial planners can determine whether they must seek additional funding from sources outside the firm.

Usually the budgeting process begins with the construction of individual budgets for sales and for each of the various types of expenses: production, human resources, promotion, administration, and so on. Budgeting accuracy is improved when budgets are first constructed for individual departments and for shorter periods of time. These budgets can easily be combined into a com-

panywide cash budget. In addition, departmental budgets can help managers monitor and evaluate financial performance throughout the period covered by the overall cash budget.

Most firms today use one of two approaches to budgeting. In the traditional approach, each new budget is based on the dollar amounts contained in the budget for the preceding year. These amounts are modified to reflect any revised goals, and managers must justify only new expenditures. The problem with this approach is that it leaves room for the manipulation of budget items to protect the (sometimes selfish) interests of the budgeter or his or her department.

This problem is essentially eliminated through zero-base bud geting.

Zero-base budgeting is a budgeting approach in which every expense must be justified in every budget. It can dramatically reduce unnecessary spending. However, some managers feel that zero-base budgeting requires too much time-consuming paperwork.

3. Identifying Sources of Funds. The four primary sources of funds are sales revenue, equity capital, debt capital, and the sale of assets. Future sales generally provide the greatest part of a firm's financing.

Sales revenue is the first type of funding.

The second type of funding is equity capital, which is money received from the sale of shares of ownership in the business. Equity capital is used almost exclusively for long-term financing. Thus it might be used to start a business and to fund expansions or mergers. It would not be considered for short-term financing needs.

The third type of funding is debt capital, which is money obtained through loans. Debt capital may be borrowed for either short- or long-term use.

The fourth type of funding is the sale of assets. A firm generally acquires assets because it needs them for its business operations. Therefore, selling assets is a drastic step. However, it may

|

|

be a reasonable last resort when neither equity capital nor debt capital can be found. Assets may also be sold when they are no longer needed.

MONITORING AND EVALUATING FINANCIAL PERFORMANCE

It is important to ensure that financial plans are being implemented and to catch minor problems before they become major problems. Accordingly, the financial manager should establish a means of monitoring and evaluating financial performance. Interim budgets (weekly, monthly, or quarterly) may be prepared for comparison purposes. These comparisons point up areas that require additional or revised planning.

|

|

|

|

Exercises

I. Translate into Russian.

Basis of financial management; goal; objective; sources of fi

nancing; funding; step; important task; financial performance;

budgeting; expenditure; revenue; sales revenue; equity capital;

debt capital; specific period; profit; assets; short-term borrowing;

long-term borrowing; merger; companywide budget; cash budget;

zero-base budgeting; income; source; share of ownership; assign

a cost; justify; meet needs; obtain; implement; modify; establish;

reduce; determine; evaluate. !:

II. Find the English equivalents. \

Финансовый план; бюджет; составление бюджета; наличный бюджет; бюджет всей компании; промежуточный бюджет; доход (годовой); доход; доход от продаж; заемный капитал; работа фирмы; активы; бюджетная статья; расход; источник денежных средств; доля собственности; акционерный капитал; средство; последнее спасительное средство; радикальный шаг; финансовая деятельность; определять стоимость; решать; оценивать; оправдывать; осуществлять; удовлетворять потребности; нести издержки; финансировать; занимать (брать в долг).

III. Fill in the blanks.

1. Financial planning begins with the establishment of ... and

2. A budget is a financial statement that projects ... and/or ... over a specified future period of time.

3. Usually the budgeting process begins with the construction of individual budgets for each of the various types of ... .

4. Budgeting accuracy is improved when budgets are first constructed for individual ... for shorter periods of time.

5. Departmental budgets can help managers .. . and financial performance throughout the period covered by the overall cash budget.

6. In the traditional approach, each new budget is based on the ... contained in the budget for the .. . year.

7. This approach leaves room for the manipulation of ... ...

to protect the interests of separate departments.

8. Zero-base budgeting is a budgeting approach in which every ... must be justified in every budget.

9. ... ... are the first type of funding.

10. The second type of funding is .......

11. The third type of funding is .......

12. The fourth type of funding is the ... of ....

13. Selling assets is a ... ... .

14. The financial manager should establish a ... of monitoring and ... financial performance.

IV. Translate into English in a written form.

1. Финансовый план—это план получения и использования денег, необходимых для осуществления целей организации.

2. Финансовое планирование начинается с установления конечных целей и поэтапных целей.

3. Бюджет предусматривает доход и расходы за конкретный период времени.

4. Процесс составления бюджета (budgeting) начинается с составления отдельных бюджетов по продажам и по каждому виду расходов.

5. Эти бюджеты легко объединяются в наличный бюджет всей компании.

6. Многие фирмы используют один из двух подходов к построению бюджетов.

7. При традиционном подходе новый бюджет основывается на бюджете за предыдущий год и руководители обосновывают только новые расходы.

8. Это оставляет место для манипуляции бюджетными статьями.

9. Эта проблема в основном ликвидируется через бюдже

тирование нуля. -;••;

10. Четырьмя основными источниками финансирования являются: доход от продаж, акционерный капитал, заемный капитал и продажа активов.

11. Продажа активов — это последнее спасительное средство.

12. Финансовый руководитель должен обеспечить (establish) средство контроля и оценки финансовой деятельности.

V. Questions and assignments.

1. What is a plan?

2. What is a financial plan?

3. What does financial planning begin with?

4. State the difference between goals and objectives.

5. List the three steps involved in financial planning.

6. In what case financial planning cannot proceed?

7. State the meaning of the word "budget".

8. Give the examples of various types of expenses which must be considered (учтены) in budgeting process?

9. How can budgeting accuracy be improved?

10. What is the peculiarity (особенность) of the traditional approach to budgeting?

11. What is the problem with this approach?

12. What is the difference between the traditional budgeting approach and zero-base budgeting?

13. What is the problem with zero-base budgeting?

14. List the four primary sources of funding.

15. For what purpose (цель) is equity capital used?

16. Is selling assets a normal step?

17. In what case selling assets may be a reasonable last resort?

18. For what purpose may interim budgets be prepared?

VI. Make up a written abstract (краткое изложение) of the text.

VII. Retell the prepared abstract.

Unit 5

Outside Sources of Financing

Financial management consist of all those activities that are concerned with obtaining money and using it effectively. Effective financial management involves careful planning. It begins with a determination of the firm's financial needs.

Money is needed to start a business. Then the income from sales could be used to finance the firm's continuing operations and to provide a profit.

But sales revenue does not generally flow evenly. Income and expenses may very from season to season or from year to year. Temporary financing may be needed when expenses are high or income is low. Then, the need to purchase a new facility or expand an existing facility may require more money than is available within a firm. In these cases the firm must look for outside sources of financing. Usually it is short- or long-term financing.

1. Short-term financing is money that will be used for one year or less and then repaid.

There are many short-term financing needs. Two deserve special attention. First, certain necessary business practices may affect a firm's cashflow and create a need for short-term financing.

Cashflow is the movement of money into and out of an organization. The ideal is to have sufficient money coming into the firm, in any period, to cover the firm's expenses during that period. But the ideal is not always achieved. For example, a firm that offers credit to its customers may find an imbalance in its cash flow. Such credit purchases are generally not paid until thirty or sixty days (or more) after the transaction. Short-term financing is then

|

|

needed to pay the firm's bills until customers have paid their bills. Unanticipated expenses may also cause a cash-flow problem.

A second major need for short-term financing that is related to a firm's cash-flow problem is inventory.

Inventory requires considerable investment for most manufactures, wholesalers, and retailers. Moreover, most goods are manufactured four to nine months before they are sold to the ultimate customer. As a result, manufacturers often need short-term financing. The borrowed money is used to buy materials and supplies, to pay wages and rent, and to cover inventory costs until the goods are sold. Then, the money is repaid out of sales revenue. Additionally, wholesalers and retailers may need short-term financing to build up their inventories before peak selling periods. Again, the money is repaid when the merchandise is sold.

2. Long-term financing is money that will be used for longer period than one year. Long-term financing is needed to start a new business. It is also needed for executing business expansions and mergers, for developing and marketing new products, and for replacing equipment that becomes obsolete or inefficient.

The amounts of long-term financing needed by large firms can be very great.

|

|

Exercises

I. Translate into Russian.

Income; profit; facility; sales revenue; expense; source; term; short-term financing; long-term financing; cash; cash flow; expand; provide; obtain; purchase; affect; be available; repay; borrow; transaction; supplies; marketing; equipment; merger; retailer; wholesaler; manufacturer; imbalance; merchandise; inventory; rent; sales revenue.

II. Find the English equivalents.

Финансовые потребности; арендная плата; стоимость; изготовитель; оптовый торговец; розничный торговец; (торговая) сделка; доход от продажи; припасы; товары; слияние (предприятий); определение; товарные запасы; оборудование; продажа; доход; прибыль; расход; срок; краткосрочное финансирование; долгосрочное финансирование; денежная наличность; движение наличности; обеспечивать; изменяться; покупать; быть в наличии; предлагать; заменять; влиять (на); конечный; устарелый; неэффективный; непредвиденный; тщательный.

III. Fill in the blanks.

1. Financial management begins with a determination of the firm's... .

2. Temporary financing may be needed when ... are high and ... is low.

3. In these cases the firm must look for outside ... of financing.

4. Short-term financing is ... that will be used for one year or less and then ....

5. Cash flow is the movement of ... into and out of an organization.

6. A firm that offers credit to its customers may find an imbalance in its ... .

7. A second major need for ... financing that is related to a firm's cash-flow problem is ... .

8. The borrowed money is used to buy ... and ... , to pay ... and to cover ... until the goods are sold.

IV. Translate into English.

1. Финансовый менеджмент состоит из тех видов деятельности (activities), которые относятся к получению денег и эффективному их использованию.

2. Краткосрочное финансирование — это деньги, которые будут использоваться в течение одного года или менее (less).

3. Существуют (there are) многие потребности краткосрочного финансирования, но движение наличности и товарные запасы представляют (are) две основные проблемы.

4. Товарные запасы требуют значительного инвестирования для большинства производителей, оптовых торговцев и розничных торговцев.

5. Занятые деньги возвращаются (is repaid) из дохода от продаж.

V.. Answer the questions.

1. Is money needed to start a business?

2. When may temporary financing be needed?

3. What kinds (виды) of financing do you know?

4. What is short-term financing?

5. What is cash flow?

6. What is the ideal cash flow?

7. What can cause a cash flow problem?

8. Does inventory require considerable investment for most manufacturers, wholesalers and retailers?

9. Why do manufacturers often need short-term financing?

10. For what purpose (цель) is the borrowed money often used by the manufacturers?

11. When is the borrowed money usually repaid?

12. What is long-term financing? , .:

13. For what purpose is long-term financing needed?

14. Are the amounts of long-term financing greater than those of short-term financing?

VI. Make up a written abstract of the above text.

VII. Retell the prepared abstract.

Unit 6

Sources of Unsecured Financing

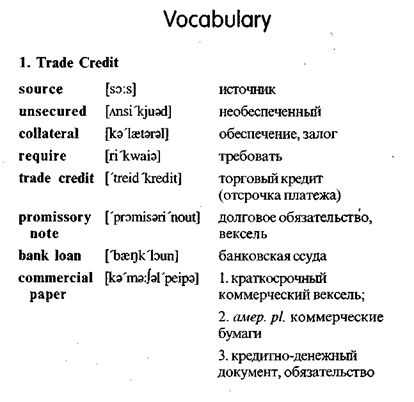

Unsecured financing is financing for which collateral is not required. Most short-term financing is unsecured. Sources of unsecured short-term financing include trade credits, promissory notes, bank loans, commercial papers, and commercial drafts.

1. TRADE CREDIT

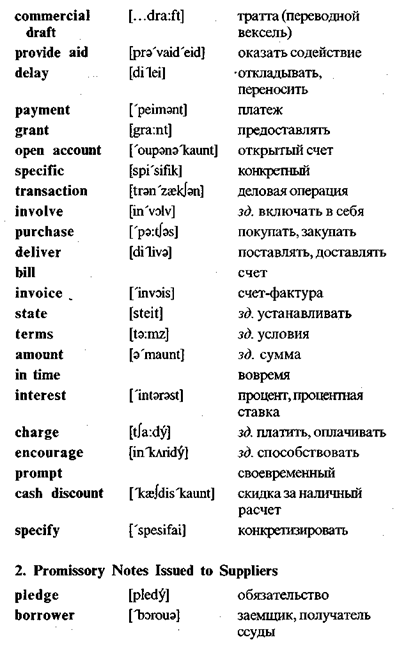

Wholesalers may provide financial aid to retailers by allowing them thirty to sixty days (or more) in which to pay for merchandise. This delayed payment, which may also be granted by manufacturers, is a form of credit known as trade credit or the open account. More specifically, trade credit is a payment delay that a supplier grants to its customers.

Between 80 and 90 percent of all transactions between businesses involve some trade credit. Typically, the purchased goods are delivered along with a bill (or invoice) that states the credit terms. If the amount is paid on time, no interest is generally charged. In fact, the seller may offer a cash discount to encour-. age prompt payment. The terms of a cash discount are specified on the invoice.

2. PROMISSORY NOTES ISSUED TO SUPPLIERS

A promissory note is a written pledge by a borrower to pay a certain sum of money to a creditor at a specified future date. Unlike trade credit, however, promissory notes usually require the borrower to pay interest. Although repayment periods may extend to one year, most promissory notes specify 60 to 180 days. The customer buying on credit is called the maker and is the party that

issues the note. The business selling the merchandise on credit is called the payee.

A promissory note offers two important advantages to the firm extending the credit. First, a promissory note are negotiable instruments that can be sold when the money is needed immediately.

3. UNSECURED BANK LOANS

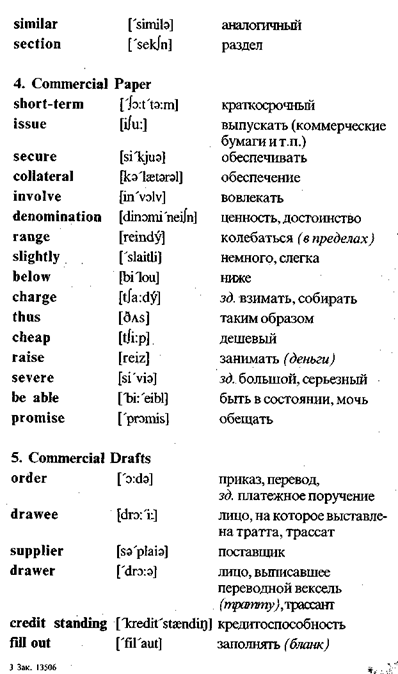

Commercial banks offer unsecured short-term loans to their customers at interest rates that vary with each borrower's credit rating. The prime interest rate (sometimes called the preference rate) is the lowest rate charged by a bank for a short-term loan. This lowest rate is generally reserved for large corporations with excellent credit ratings. Organizations with good to high credit ratings may have to pay the prime rate plus 4 percent. Of course, if the banker feels loan repayment may be a problem, the borrower's loan application may be rejected.

Banks generally offer short-term loans through promissory notes. Promissory notes that are written to banks are similar to those discussed in the last section.

4. COMMERCIAL PAPER

A commercial paper is a short-term promissory note issued by a large corporations. A commercial paper is secured only by the reputation of the issuing firm; no collateral is involved. It is usually issued in large denominations, ranging from $5,000 to $100,000. Corporations issuing commercial papers pay interest rates slightly below those charged by commercial banks. Thus, issuing a commercial paper is cheaper than getting short-term financing from a bank.

Large firms with excellent credit reputations can quickly raise large sums of money. They may issue commercial paper totaling millions of dollars. However, a commercial paper is not without risks. If the issuing corporation later has severe financing problems, it may not be able to repay the promised amounts.

|

|

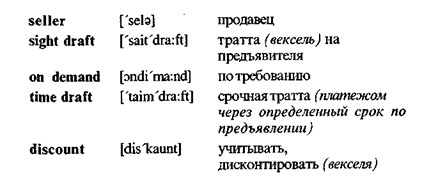

5. COMMERCIAL DRAFTS

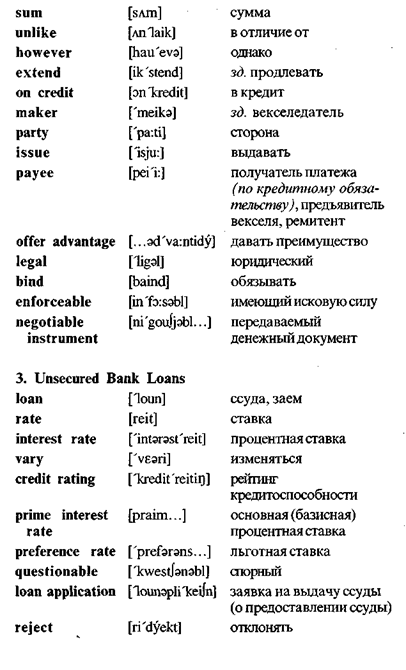

A commercial draft is a written order requiring a customer (the drawee) to pay a specified sum of money to a supplier (the drawer) for goods or services. It is often used when the supplier is insure about the customer's credit standing.

In this case, the draft is similar to an ordinary check with one exception: The draft is filled out by the seller and not the buyer. A sight draft is a commercial draft that is payable on demand -whenever the drawer wishes to collect. A time draft is a commercial draft on which a payment date is specified. Like promissory notes, drafts are negotiable instruments that can be discounted or used as collateral for a loan.

|

|

|

|

|

|

Exercises

I. Translate into Russian.

Source; unsecured financing; promissory note; commercial draft; trade credit; loan; commercial paper; transaction; delayed payment; credit terms; pay interest; interest rate; invoice; amount; prompt payment; written pledge; sum of money; borrower; repayment period; buy on credit; deliver; provide aid; maker; payee; offer loans; credit rating; prime interest rate; questionable credit rating; large denomination; raise large sums of money; drawee; drawer; credit standing; sight draft; time draft; collateral; commercial draft.

II. Find the English equivalents.

Ссуда; давать ссуду; процент; процентная ставка; необеспеченное финансирование; покупать в кредит; условия кредита; счет-фактура; основная сумма; деловая операция; торговый кредит; долговое обязательство; коммерческая бумага; тратта (переводной вексель); условия; обеспечение (за лог) ; заемщик; трассат (лицо, на которое выставлена трат та); трассант (лицо, выписавшее переводной вексель- тратту) ; кредитоспособность; тратта (вексель) на предъявителя; срочная тратта.

III. Fill in each blank with a suitable word or word combi nation.

1. Trade credit is a payment... that a supplier grants to its customers.

2. The invoice that's ....

3. A promissory note is a written ... by a borrower to pay a certain sum of money at a specified date.

. 4. The customer buying on credit is called ... and is the party that issues the promissory note.

5. The business selling the merchandise on credit is called ....

6. Most promissory notes are... that can be sold when money is needed immediately.

7. The prime interest rate is the lowest rate charged by a bank for... loan.

8. A commercial paper is ... issued by a large corporation.

9. A commercial paper is secured only by the ... of the issuing . firm.

10. Issuing a commercial paper is ... than getting short-term financing from a bank.

11. A commercial draft is a written... requiring a drawee to pay a specified sum of money to the ... for goods or services.

12. A sight draft is a commercial draft that is payable on ....

13. A ... is a commercial draft on which a payment date is specified. 14. Like promissory notes drafts can be used as ... for a loan.

IV. Translate into English.

1. Источники необеспеченного краткосрочного финансирования включают торговые кредиты, долговые обязательства, банковские ссуды, краткосрочные долговые обязательства (кредитно-денежные документы) и тратты (переводные векселя).

2. Торговый кредит — это отсрочка платежа, которую поставщик предоставляет своим клиентам.

3. Долговое обязательство — это письменное обязательство заемщика уплатить определенную сумму денег кредитору.

4. В отличие от торгового кредита долговые обязательства требуют, чтобы заемщик платил проценты.

5. Коммерческие банки предоставляют необеспеченные краткосрочные ссуды своим клиентам, которые меняются в зависимости от (with) кредитоспособности каждого заемщика.

6. Коммерческая бумага — это краткосрочное долговое обязательство, выпускаемое крупными корпорациями. .

7. Коммерческая бумага не имеет специального (special) обеспечения.

8. Тратта (переводной вексель) — это письменный приказ, требующий, чтобы трассат (лицо, на которое выставле на тратта) уплатил конкретную сумму денег поставщику за товары или услуги.

9. Тратта часто используется, когда поставщик не уверен в кредитоспособности клиента.

V. Answer the questions.

1. What is unsecured financing?

2. What are the sources of unsecured short-term financing?

3. What is a trade credit?

4. What is the difference between a promissory note and trade credit?

5. In what case a loan application may be rejected by a bank?

6. What is a commercial paper secured by?

7. Why issuing a commercial paper is cheaper than getting short-term financing from a bank?

8. What is a commercial draft?

9. Can commercial drafts be used as collaterals for loans?

VI. Make up a written abstract of the above text.

VII. Retell the prepared abstract.

Unit7

Accounting

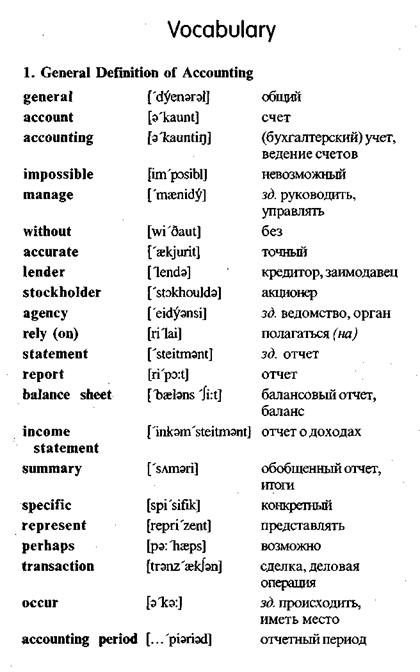

1. GENERAL DEFINITION OF ACCOUNTING

Today, it is impossible to manage a business operation without accurate and timely accounting information. Managers and employees, lenders, suppliers, stockholders, and government agencies all rely on the information contained in two financial statements. These two reports — the balance sheet and the income statement — are summaries of a firm's activities during a specific time period. They represent the results of perhaps tens of thousands of transactions that have occurred during the accounting period.

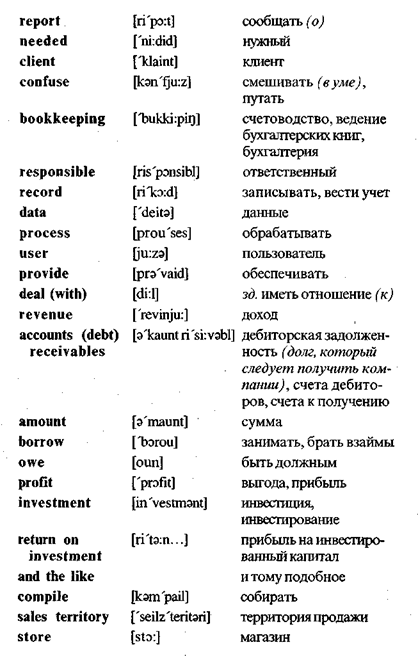

Accounting is the process of systematically collecting, an alyzing, and reporting financial information. The basic product that an accounting firm sells is information needed for the clients.

Many people confuse accounting with bookkeeping. Bookkeeping is a necessary part of accounting. Bookkeepers are responsible for recording (or keeping) the financial data that the accounting system processes.

The primary users of accounting information are managers. The firm's accounting system provides the information dealing with revenues, costs, accounts receivables, amounts borrowed and owed, profits, return on investment, and the like. This information can be compiled for the entire firm; for each product; for each sales territory, store, or individual salesperson; for each division or department; and generally in any way that will help those who manage the organization. Accounting information helps man-

agers plan and set goals, organize, motivate, and control. Lenders and suppliers need this accounting information to evaluate credit risks. Stockholders and potential investors need the information to evaluate soundness of investments, and government agencies need it to confirm tax liabilities, confirm payroll deductions, and approve new issues of stocks and bonds. The firm's accounting system must be able to provide all this information, in the required form.

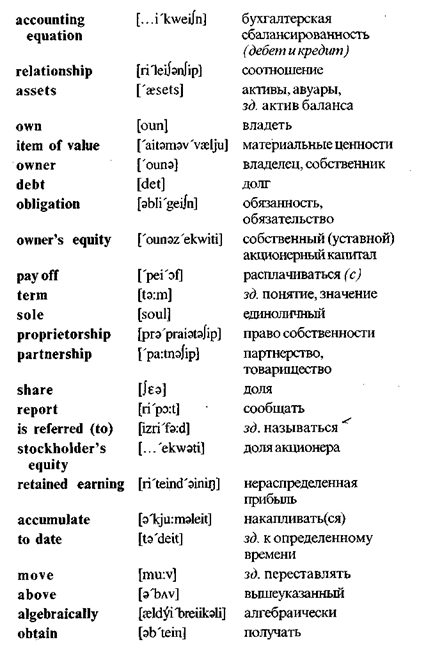

2. THE BASIS FOR THE ACCOUNTING PROCESS

The basis for the accounting process is the accounting equation. It shows the relationship among the firm's assets, liabilities, and owner's equity.

Assets are the items of value that a firm owns — cash, inventories, land, equipment, buildings, patents, and the like.

Liabilities are the firm's debts and obligations — what it owes to others.

Owner's equity is the difference between a firm's assets and its liabilities — what would be left over for the firm's owners if its assets were used to pay off its liabilities.

The relationship among these three terms is the following:

Owners' equity = assets - liabilities

(The owners' equity is equal to the assets minus the liabilities)

For a sole proprietorship or partnership, the owners' equity is shown as the difference between assets and liabilities. In a partnership, each partner's share of the ownership is reported separately by each owner's name. For a corporation, the owners' equity is usually referred to as stockholders ' equity or sharehold ers'equity. It is shown as the total value of its stock, plus retained earnings that have accumulated to date.

By moving the above three terms algebraically, we obtain the standard form of the accounting equation:

Assets = liabilities + owners' equity

(The assets are equal to the liabilities plus the owners' equity)

3. A BALANCE SHEET

A balance sheet (or statement of financial position), is a summary of a firm's assets, liabilities, and owners' equity ac counts at a particular time, showing the various money amounts that enter into the accounting equation. The balance sheet must demonstrate that the accounting equation does indeed balance. That is, it must show that the firm's assets are equal to its liabilities plus its owners' equity. The balance sheet is prepared at least once a year. Most firms also have balance sheets prepared semi-annually, quarterly, or monthly.

4. AN INCOME STATEMENT

An income statement is a summary of a firm's revenues and expenses during a specified accounting period. The income statement is sometimes called the statement of income and expenses. It may be prepared monthly, quarterly, semiannually, or annually. An income statement covering the previous year must be included in a corporation's annual report to its stockholders.

5. THE IMPORTANCE OF THE ABOVE TWO STATEMENTS

The information contained in these two financial statements becomes more important when it is compared with corresponding information for previous years, for competitors, and for the industry in which the firm operates. A number of financial ratios can also be computed from this information. These ratios provide a picture of the firm's profitability, its short-term financial position, its activity in the area of accounts receivables and inventory, and its long-term debt financing. Like the information on the firm's financial statements, the ratios can and should be compared with those of past accounting periods, those of competitors, and those representing the average of the industry as a whole.

|

|

|

|

|

|

|

|

|

|

Exercises

I. Translate into Russian.

Accounting; bookkeeping; accounting information; lender; stock; stockholder; financial statement; balance sheet; income statement; assets; liabilities; owners' equity; bond; debt; annual report; profitability; accounting period; return on investment; soundness of investment; issue of stocks and bonds; revenue; profit; account receivable; transaction; amount; own; owner; relay on; report; borrow; deal with; confirm; approve; provide; compare.

II. Find the English equivalents.

Бухгалтерский учет (бухучет); точная и своевременная информация; акционер;кредитор; ведомство (агентство); отчет

(доклад); балансовый отчет; отчет о доходах; отчетный период; счетоводство (бухгалтерия) ; финансовая информация; прибыль (доход) ; выгода (прибыль) ; прибыль на инвестированный капитал; дебиторская задолженность; обязательство; денежное обязательство (пассив); платежная ведомость; акция (ценная бумага); активы; долг; счет прибылей (иубыт ков); ежегодный отчет; доходность; собственный акционерный капитал; одобрять; сравнивать; подтверждать; занимать (брать взаймы); обрабатывать (информацию).

III. Fill in the blanks.

1. Managers, lenders, suppliers and government agencies relay on the information contained in two ....

2. These two reports — the balance sheet and ... — are summaries of a firm's activities during a specific time period.

3. The basis for the accounting process is ....

4. Assets are the ... that a firm owns.

5. Liabilities are the firm's debts and ....

6. Owners' equity is the difference between a firm's ... and its liabilities.

7. A balance sheet is ... of a firm's assets, liabilities, and owners' equity accounts at a particular time.

8. A balance sheet must demonstrate that the accounting ... does indeed balance.

9. An income statement is a summary of a firm's revenues and

... during a specific accounting period. >

10. The information in these two financial statements becomes

more important when it is... with corresponding information

for previous years or past... periods.

IV. Translate into English.

1. Бухгалтерский учет — это процесс систематического сбора и сообщения финансовой информации.

2. Балансовый отчет и отчет о доходах являются (are) основой процесса бухучета.

3. Балансовый отчет (или отчет о финансовом положении) — это (is) обобщенный отчет об активах фирмы, пассивах и собственном акционерном капитале.

4. Отчет о доходах — это обобщенный отчет о доходах и расходах за (during) конкретный отчетный период.

5. Основой процесса бухгалтерского учета является буху-четное уравнение.

6. Согласно (according to) бухучетному уравнению активы равны пассивам (денежным обязательствам) плюс собственный акционерный капитал.

7. Собственный акционерный капитал—это разность между активами и пассивами.

8. Балансовый отчет должен показывать, что бухучетное уравнение балансируется.

9. Результаты (results) балансового отчета должны сравниваться (be compared) с результатами за (for) прошлый отчетный период.

10. Эта информация дает картину доходности фирмы, ее финансового положения и ее деятельности в области (area) дебиторской задолженности, товарных запасов и долгового финансирования.

V. Questions and assignments.

1. What is accounting? Give a short definition.

2. Is it possible to manage a business operation without accurate and timely accounting information?

3. Who needs accounting information? Explain why.

4. What is the basis for accounting process?

5. State (изложите) the standard form of the accounting equation.

6. What is a balance sheet? Give a short definition.

7. What must a balance sheet show?

8. What is an income statement?

9. What can be computed from the information contained in a balance sheet and an income statement?

|

|

10. Do the ratios computed from this information provide a picture of a firm's profitability and its financial position?

11. Is this information for competitors?

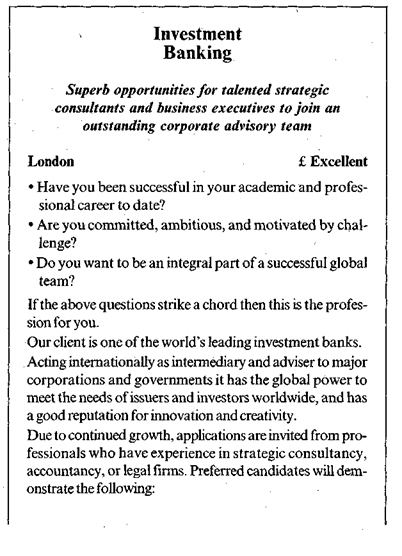

VI. Read and translate this newspaper advertisement.

|

|

|

|

|

|

VII. Answer the questions.

1. What is the name of the firm that has published this ad (advertisement)?

2. Who is the firm's client?

3. What information have you got about the bank for which the firm works?

4. What kind of (каких) specialists does the firm invite?

5. What kind of experience must the invited professionals have?

6. Does experience in accountancy matter (имеет значение )1

7. What will preferred candidates demonstrate?

8. What chief traits (основные черты) of character must the applicants have?

9. Is it necessary to send a full curriculum vitae to Michael Page City firm?

10. What words in the ad characterize the team within which the selected applicants will work?

Unit 8

Operations Management

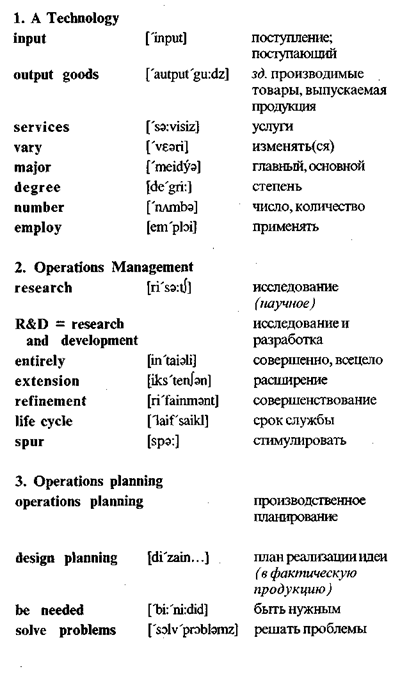

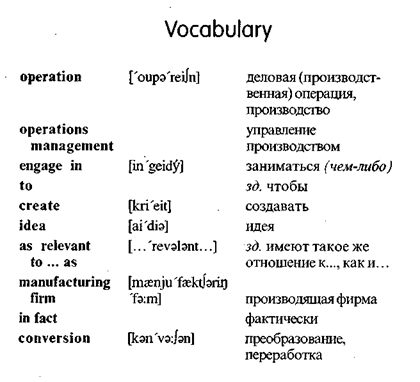

Operations management consists of all the activities that managers engage in to create products (goods, services, and ideas). Operations are as relevant to service organizations as to manufacturing firms. In fact, production is the conversion of resources into goods or services.

1. A technology is the knowledge and process the firm uses to convert input resources into output goods or services. Conversion processes vary in their major input, the degree to which inputs are changed, and the number of technologies employed in the conversion.

2. Operations management often begins with the research and product development activities. The results of R&D may be entirely new products or extensions and refinements of existing products. The limited life cycle of every product spurs companies to invest continuously in R&D.

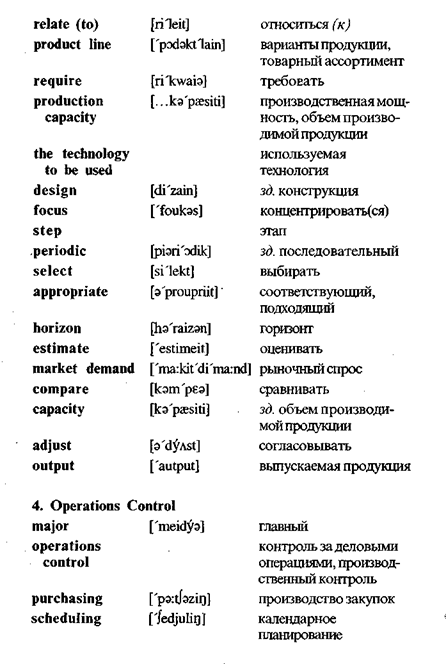

3. Operations planning is planning for production. First, design planning is needed to solve problems related to the product line, required production capacity, the technology to be used, the design of production facilities, and human resources. Next, operational planning focuses on the use of production facilities and resources. The steps in this periodic planning are (1) selecting the appropriate planning horizon, (2) estimating market demand, (3) comparing demand and capacity, and (4) adjusting output to demand.

4. The major areas of operations control are purchasing, inventory control, scheduling, and quality control. Purchasing in-

|

|

volves selecting suppliers and planning purchases. Inventory control is the management of stocks of raw materials, work process, and finished goods to minirnize the total inventory cost. Scheduling ensures that materials are at the right place at the right time — for use within the facility or for shipment to customers. Quality control ensures that products meet their design specifications.

5. Automation, the total or near-total use of machines to do work, is rapidly changing the way work is done in factories and offices. A growing number of industries are using programmable machines called robots to perform tasks that are tedious or hazardous to human beings. The flexible manufacturing system combines robotics and computer-aided manufacturing to produce smaller batches of products more efficiently than the traditional assembly line.

|

|

|

|